|

Listen to this article here

Getting your Trinity Audio player ready...

|

In the financial heartland of the United States, the Navy Federal Credit Union (NFCU) stands as a colossus. Boasting over $165 billion in assets and serving a vast membership of about 13 million, NFCU is not just any financial institution; it is the largest credit union in the nation, a financial giant whose reach extends across the breadth of the American landscape.

Yet, beneath this facade of financial might and inclusivity lies a stark, all too predictable, deep-seated racial disparity in mortgage approvals that cuts to the core of the systemic injustices still prevalent in our society.

At the heart of this controversy is the disturbing revelation of the Navy Federal Credit Union and its lending practices, which have laid bare the unyielding grip of white supremacy in even the most trusted financial institutions.

Recent investigations have brought to light a harrowing gap in mortgage approval rates between Black and White borrowers. This gap speaks volumes about the insidious denial of Black livelihood this company maintains while raking in billions.

The numbers are more than just statistics; they are a stark reminder of the ongoing struggle against a legacy of poverty and suffering. The disparity in mortgage approvals is not just a matter of financial inequity; it is a powerful indictment of the financial system’s systemic racism that continues to undermine the shortened lives and lessen the happiness of Black Americans.

In a nation where homeownership is often synonymous with the American Dream, the denial of this opportunity to Black applicants is a grim testament to the pervasive inequalities that remain a blight on the nation’s conscience.

The Disparity in Numbers: A Stark Contrast in Mortgage Approvals at Navy Federal Credit Union

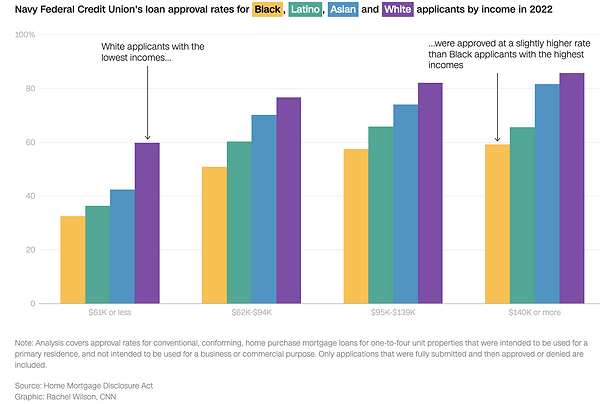

In 2022, the numbers paint a troubling picture of disparity: 77.1% of White applicants received approval for their mortgage applications. This figure stands in glaring contrast to the 55.8% approval rate for Latino applicants and an even more dismal 48.5% for Black applicants. This discrepancy highlights a significant racial gap and raises serious concerns about systemic biases embedded within the lending practices of one of the nation’s most prominent financial institutions.

Further intensifying this troubling scenario is the fact that NFCU rejected approximately 3,700 Black applicants for home purchase mortgages in the same year. This high number of rejections is not just a statistic; it represents thousands of dreams deferred by thousands of individuals and families whose aspirations for homeownership were curtailed. This is particularly poignant in a year marked by rising interest rates, which already pose a significant barrier to home buying.

For Black applicants, who historically have faced systemic hurdles in accumulating wealth and accessing financial opportunities, these rejections add another layer of emotional devastation, deepening are suffering.

Broader Implications and National Context

The disparities in mortgage approval rates at Navy Federal Credit Union (NFCU) are not an isolated phenomenon but rather a reflection of a more significant national issue concerning the widening homeownership gap between White and Black Americans. This gap is a stark manifestation of the enduring racial hatred maintained by individuals and institutions in the United States, particularly in the realm of financial access and opportunities.

When looking at other significant lenders like Wells Fargo, US Bank, and Bank of America, NFCU’s racial approval rate gaps provide an insightful perspective into how widespread these issues are within the financial sector.

While everyone knows disparities exist across all financial institutions, the extent and nature of these gaps can vary. Navy Federal Credit Union and its particularly stark contrast in approval rates highlight the need for a sector-wide examination and reform of lending practices to address these deeply rooted inequities.

More Stories

Conclusion: A Call to Action for Equity and Justice in Mortgage Lending

In a society where white individuals predominantly hold political power and influence, it becomes a moral imperative for those white folks in positions of authority and influence to actively work toward dismantling these systemic barriers.

The responsibility to address and rectify these disparities should not rest solely on the shoulders of those who are most affected by them. Instead, it requires a concerted effort from all sectors of society, especially from those who have the means to effectuate meaningful change.

White people, particularly those in positions of power in the financial sector and government, must acknowledge the role they play in perpetuating these disparities, either through action or inaction.

Moving beyond mere acknowledgments of the problem, it is essential to implement concrete measures that ensure fair and equitable lending practices. This includes revising policies, enhancing regulatory oversight, and actively working to eliminate biases in lending processes.

An original version of the Navy Federal Credit Union article can be found at the Unapologetic Black Newsletter.

Leave a comment